New Year, New Tax Law: How OBBBA Reshapes Individual Taxes in 2025

- Jan 4

- 3 min read

2025 is a game-changing year for tax planning. The One Big, Beautiful Bill Act (“OBBBA”), signed into law on July 4, 2025, makes the most sweeping changes to the tax code since the Tax Cuts and Jobs Act (TCJA). As we kick off a new year, Seiberling & Company is excited to announce our Weekly OBBBA Spotlight—a blog series unpacking the most impactful provisions of this new law so you can take full advantage in your 2025 tax planning.

This week, we start with what matters most to individuals and families: the headline changes for personal tax returns, deductions, and credits.

What’s New for Individuals Under OBBBA (2025 and Beyond)

Permanent Lower Tax Rates & Bigger Standard Deduction

TCJA’s reduced tax rates and expanded income brackets are now permanent. No more scheduled “snap back” to pre-2018 higher rates.

Marriage penalty relief remains in place for joint filers (except at the top bracket).

The standard deduction is increased and will be indexed for inflation from a new base year, providing more upfront tax relief for most filers.

SALT Deduction Cap & Pease Limitation

The state and local tax (SALT) deduction cap jumps to $40,000 for 2025, with phaseouts for high-income taxpayers. The cap will revert to $10,000 in 2030 unless new legislation intervenes.

The Pease limitation on itemized deductions is repealed, replaced by a much smaller 2% reduction for very high earners.

Enhanced Child Tax Credit & Other Dependent Credit

Child tax credit is now $2,200 per child (indexed for inflation), with stricter Social Security number requirements for both taxpayers and qualifying children.

Credit for other dependents ($500) is made permanent.

New Temporary Deductions

Tips: Deduct up to $25,000 per year in tips if you work in occupations where tipping is customary—even if you don’t itemize.

Overtime Pay: Deduct up to $12,500 in qualified overtime pay (phased out for higher incomes).

Car Loan Interest: For 2025–2028, deduct up to $10,000 of interest paid on new U.S.-assembled vehicle loans, subject to income limits and documentation.

Expanded Credits & Deductions

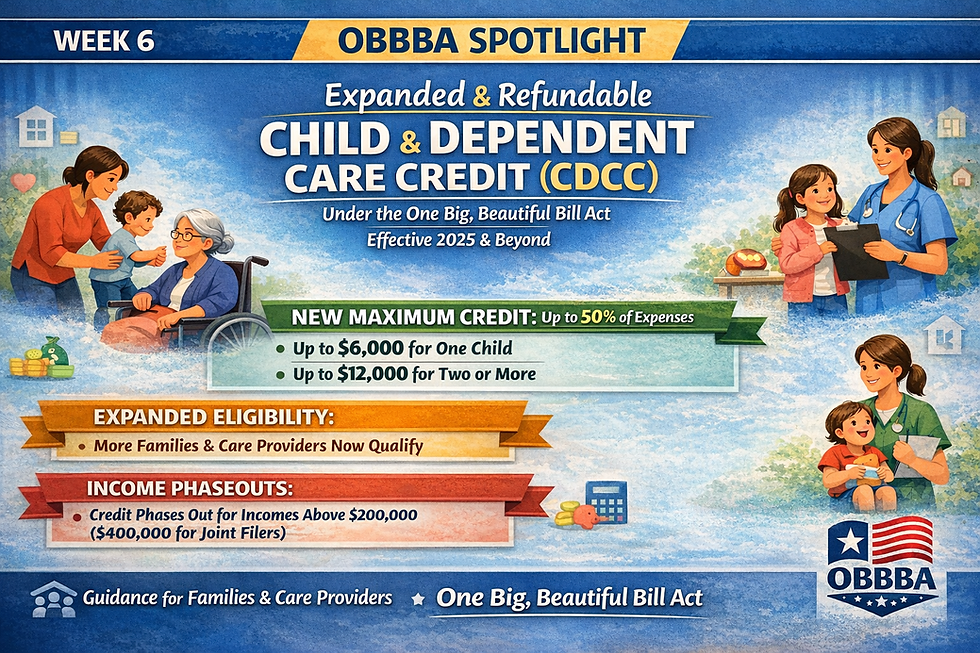

Child and Dependent Care Credit: Maximum credit rate increases to 50%, with expanded eligibility and higher phaseout thresholds.

School Choice Credit: Up to $1,700 credit for contributions to qualified scholarship-granting organizations in participating states.

Adoption Credit: Now refundable up to $5,000 (indexed for inflation).

Trump Accounts for Children: New tax-deferred investment accounts for children, with a $1,000 federal seed contribution for newborns through 2028.

Charitable Giving: New 0.5% of AGI floor for itemized deductions; non-itemizers can deduct up to $1,000 ($2,000 for joint filers) above the line.

Other Notable Changes

Personal exemptions remain suspended for most, but a $6,000 senior deduction is available for those age 65+ through 2028.

Mortgage interest deduction cap of $750,000 is now permanent, and mortgage insurance premiums are always deductible.

Casualty losses are now limited to federally or state-declared disasters.

Miscellaneous itemized deductions remain suspended (except for unreimbursed educator expenses).

Weekly OBBBA Spotlight: Upcoming Topics

Here’s what to expect in the coming weeks:

Week | Topic |

1 | Permanent Lower Tax Rates & Standard Deduction |

2 | Child Tax Credit & Other Dependent Credit: Enhancements and Eligibility |

3 | SALT Cap Increase & Pease Limitation Repeal |

4 | New Deductions for Tips and Overtime |

5 | Car Loan Interest Deduction: Rules and Planning |

6 | Expanded & Enhanced Credits: Child/Dependent Care, Adoption, School Choice |

7 | Charitable Contributions: New AGI Floor & Above-the-Line Deduction |

8 | Mortgage & Casualty Loss Deductions: Permanent & Temporary Changes |

9 | Senior Deduction, Personal Exemptions, Miscellaneous Itemized Deductions |

10 | Section 179 Expensing and 100% Bonus Depreciation (for business owners) |

11 | Qualified Business Income (QBI) Deduction: Permanent Rules and Expansion |

Note: Business-specific changes will be addressed in our next blog post and in Weeks 10–11.

Take Action

As always, proactive planning is the key to maximizing your tax benefits. If you have questions about how these provisions impact your situation, please contact our team—we’re here to help you navigate this new environment with confidence.

Stay tuned!

Comments